Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

How Buying a Multi-Generational Home Helps with Affordability Today

In today’s world of rising housing costs, many buyers are looking for ways to still be able to buy a home. Some of them have found a solution in multi-generational living.

Multi-generational living is when two or more adult generations live together under one roof. This includes siblings, parents, or even grandparents. Here’s an in-depth look at why more buyers are choosing this option today, so you can see if it may be right for you too.

Reasons To Buy a Multi-Generational Home

According to a recent study by the National Association of Realtors (NAR), the top two reasons people are opting for multi-generational homes today have to do with affordability (see graph below):

Cost Savings: About 28% of first-time buyers and 11% of repeat buyers are deciding on a multi-generational home to save on costs. By pooling their resources, households can share the financial responsibilities like mortgage payments, utilities, property taxes, and maintenance, to make homeownership more affordable. This is especially helpful for first-time homebuyers who may be finding it tough to afford a home on their own in today’s market.

More Space: Another 28% of first-time buyers and 18% of repeat buyers are doing it because they want a larger home they couldn’t afford on their own. For some of the repeat buyers who listed this as a main motivator, it could be because they find themselves taking care of older parents while also welcoming back young adults who’ve returned to the nest. With everyone chipping in and combining their incomes, suddenly, that big dream home with more space is within reach. As the Triangle Business Journal explains:

“Choosing multi-gen living allows people to purchase a home much larger than they could afford on their own by leveraging the combined income, credit and a down payment of those that they will be occupying the home with.”

Lean on an Expert

If you’re interested in this too, partner with a local real estate agent. Finding the perfect multi-generational home isn’t as simple as shopping for a regular house. That’s because there are more people with even more opinions and needs that should be considered.

You’ve got to make sure everyone has their own space, find room for shared household time, and possibly even create adaptable areas for older relatives. It’s a puzzle, and the pieces need to fit just right. Your real estate agent has the expertise and local knowledge to help you find that home where everyone can be comfortable without breaking the bank. As MoneyGeek.com puts it:

“Having a good multigenerational property can improve the prospects of success when living with loved ones. A multigenerational home should fit the specific needs of most family members regardless of age or health. Speaking to a real-estate agent can help you gain clarity and locate a fit.”

Bottom Line

Buying a multi-generational home can be a smart way to tackle some of today’s affordability challenges. When you team up to share expenses, you can make your dream of homeownership more attainable. If this sounds like an option for you and your loved ones, let’s connect to help you find a home that’s the perfect fit.

The Difference Between Renting and Buying a Home

Some Highlights

- When deciding between buying a home or renting, think about these three important factors.

- Buying a home means avoiding rising rents, owning a tangible and valuable asset, and growing your wealth over time.

- If you’re ready to enjoy the advantages of owning a home, let’s connect to discuss your options.

Growing Your Net Worth with Homeownership

Take a moment to imagine where you want to be in a few years. You might be thinking about your job, money, wanting more stability, or goals you want to reach soon. Is homeownership a part of that vision? If it is, you should know owning a home has a whole lot of financial benefits.

One of the many reasons to buy a home is that it’s a great way to build wealth and gain financial stability. That’s because the value of most homes increases over time, which in turn grows your net worth. Here’s how home values are rising right now. According to Zillow:

“The total value of the U.S. housing market – the sum of Zillow’s estimated value for every U.S. home – is now slightly less than $52 trillion, which is $1.1 trillion higher than the previous peak reached last June.”

Basically, homeownership is a tremendous wealth-building tool. And with home values back on the rise across the nation, now might be a good time to consider if owning a home is something you want to reach for.

Here’s a look at some data to see how much owning a home can really make a difference in your life.

Household Net Worth Is Rising

Data shows that while those in the top 1% saw the most dramatic net worth increase, people from every single tax bracket have seen their wealth grow over the past few years (see graph below):

For many of those people, the rising value of their home plays a big part in that.

Owning a Home Helps You Achieve Financial Success

You can tell homeownership had a lot to do with that growth because there’s a significant net worth gap between homeowners and renters. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“. . . homeownership is a catalyst for building wealth for people from all walks of life. A monthly mortgage payment is often considered a forced savings account that helps homeowners build a net worth about 40 times higher than that of a renter.”

The big reason why? Homeowner’s build equity. Home equity is the value of your home minus the amount you owe on your mortgage. And for most homeowners, that’s the largest contributor to their net worth. Here’s the data from First American to prove it (see graph below):

The blue portion of each bar represents housing as a portion of net worth – and it’s clearly a bigger contributor than other investments like stocks, gold, and cryptocurrencies. As you can see, across different income levels, homeownership does more to build the average household’s wealth than anything else.

Bottom Line

One of the biggest benefits of owning a home is that it can provide an avenue to grow your net worth. Let’s connect so you can start investing in homeownership.

Are Grandparents Moving To Be Closer to Their Grandkids?

During the pandemic, many people distanced themselves from their loved ones for health reasons. Grandparents were told to stay away from their grandkids, especially as schools started to open. That’s because it would have been risky to visit with their grandchildren who may have gotten sick from school.

Now that the pandemic has passed, many grandparents want more than ever to be near their grandchildren again to make up for that lost time. But how are they getting that “Grandparent Wish?” The data tells us many are moving to make sure they’re getting more quality time.

Grandparents Are Moving To Be Near Loved Ones

Recent data from the National Association of Realtors (NAR) shows people between the ages of 55 and 74 are moving farther (more than 100 miles) than any other age group (see graph below):

The average age of grandparents in the U.S. is 67 years. The logical leap is that at least some of the people who are moving the furthest are grandparents. But what’s causing them to move so far?

The same report from NAR shows the top reason people move is to be closer to loved ones (see graph below):

Based on this data, it’s fair to say many grandparents are getting their wish of more quality time with their grandchildren by moving to be closer to them. And after experiencing isolation and loneliness during the COVID pandemic, that’s an especially good thing.

If you’re a grandparent, you know how important your grandchildren are. And you may be willing to sell and move just to be closer by. As Vance Cariaga, a journalist at Go Bank Rates, explains:

“Never underestimate the power of grandchildren – especially when it comes to lifestyle and financial decisions. Recent data shows that many baby boomers are relocating further away from home than they used to so they can be closer to their grandbabies.”

Bottom Line

The data shows grandparents are moving further to be near their grandchildren. If you have grandchildren of your own, maybe you can relate. When you decide it’s time to be closer to your loved ones, let’s connect.

Understanding the Benefits of Owning Your First Home

Are you considering buying your first home? If so, it can be helpful to know what led other people to make that decision. According to a recent survey of first-time homebuyers by PulteGroup:

“When asked why they purchased their first home recently, the answer was simple: because they wanted to. Either the desire to stop renting or recognition that homeownership is a smart financial investment was the main motivator for 72% of respondents.”

While that survey looked specifically at first-time homebuyers buying newly built homes, the same sentiment is true for just about anyone buying their first home. Here’s a bit more information to help you think about those two benefits of homeownership to see if they’re a key factor for you too.

When You Buy a Home, You Have More Stability than When You Rent

You might want to stop renting because rents keep going up. If you’re a renter, that means there’s a chance your payment will increase each time you sign a new rental agreement or renew your current one.

On the other hand, when you buy your home with a fixed-rate mortgage, your monthly housing payment is predictable over the length of that loan. This stability can give you a peace of mind that renting just can’t provide. Jeff Ostrowski, real estate journalist, breaks it down:

“With a fixed-rate mortgage, your monthly principal and interest payment is set for as long as you keep the loan. Sign a rental lease, however, and you could see your rent rise the following year, the year after that and so on.”

When You Buy a Home, You Grow Your Wealth as Home Values Climb

Beyond that, owning a home can also be a great long-term investment. While renting may be the more affordable option right now, it doesn’t provide an avenue for you to grow your wealth over time. Mark Fleming, Chief Economist at First American, explains that’s an important distinction to consider:

“Given current dynamics, more young households may choose to rent in the near term as the cost to own, excluding house price appreciation, has unequivocally increased. Yet, accounting for house price appreciation in that cost of homeownership, whether to rent or buy will depend on where, and if, a home is likely to cost more or less in the near future.”

Basically, renting doesn’t allow you to build equity. In contrast, homeownership can help you grow your net worth as your home’s value appreciates. That’s a significant perk you can’t get if you keep renting.

When you take that into account, it may make better financial sense to buy. Most experts project home prices will continue to appreciate over the next few years at a pace that’s more normal for the market. That means when you buy a home, not only are you investing in a place to live, but you’re also investing in your financial future.

Bottom Line

If you’re ready, it can be a smart move to buy your first home instead of renting. Let’s connect so you can stabilize your housing payment and start building wealth for your future.

Home Prices Are Not Falling

Home Prices Are Not Falling

During the fourth quarter of last year, some housing experts projected home prices were going to crash in 2023. The media ran with those forecasts and put out headlines calling for doom and gloom in the housing market. All of this negative news coverage made a lot of people have doubts about the strength of the residential real estate market.

If it made you question if you should delay your own plans to move, here’s what you really need to know.

Home Prices Never Crashed

Disregard what you saw in the headlines. The actual data shows home prices were remarkably resilient and performed far better than the media would have you believe (see graph below):

This graph uses reports from three trusted sources to clearly illustrate prices have already rebounded after experiencing only slight declines nationally. That’s a far cry from the crash so many articles called for.

The declines that did happen (shown in red), weren’t drastic but were short-lived. As Nicole Friedman, a reporter at the Wall Street Journal (WSJ), says:

“Home prices aren’t falling anymore. . . The surprisingly quick recovery suggests that the residential real-estate downturn is turning out to be shorter and shallower than many housing economists expected . . .”

Even though some media coverage made a big deal about home prices pulling back, the slight correction that happened is already in the rearview mirror. Basically, this data shows you home prices aren’t falling anymore – they’re actually going back up.

What’s Next for Home Prices?

The consensus from experts is that home price growth will continue in the years ahead and is returning to normal levels for the market. That means we’ll still see home prices appreciating, just at a slower pace than the last few years – and that’s a good thing.

Some news sources will see home price growth slowing and put out stories that make you think prices are falling again. The return of misleading headlines like those is already having an impact on how homebuyers are feeling again. You can see how this affects general opinion in the Consumer Confidence Survey from Fannie Mae (see graph below):

While the percentage of Americans who think prices will fall has been slowly declining this year, the latest Consumer Confidence data indicates that’s ticked back up recently (shown in red). This change is surprising especially since the home price data shows prices are going up, not down. It tells you the impact the media still has on public opinion.

Don’t fall for the negative headlines and become part of this statistic. Remember, data from a number of sources shows home prices aren’t falling anymore.

Bottom Line

Even though the media may make things sound doom and gloom, the data shows home prices aren’t falling anymore. So, don’t let the headlines scare you or delay your plans. Let’s connect so you have a trusted resource to cut through the noise and tell you what’s really happening in our area.

Get Pre- Approved

If you’re looking to buy a home this fall, there are a few things you need to know. Affordability is tight with today’s mortgage rates and rising home prices. At the same time, there’s a limited number of homes on the market right now and that’s creating some competition among buyers. But, if you’re strategic, there are ways to navigate these waters. The first thing you’ll want to do is get pre-approved for a mortgage. That way you’ll know your numbers and can set yourself up for success from the start of your home search.

What Pre-Approval Does for You

To understand why it’s such an important step, you need to know what pre-approval is. As part of the homebuying process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you know how much money you can borrow. Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand how much you may be able to borrow. Why does this help you, especially today? With higher mortgage rates and home prices impacting affordability for many buyers right now, a solid understanding of your numbers is even more important so you can truly wrap your head around your options.

Pre-Approval Helps Show Sellers You’re a Serious Buyer

Let’s face it, there are more buyers looking to buy than there are homes available for sale and that imbalance is creating some competition among homebuyers. That means you could see yourself in a multiple-offer scenario when you make an offer on a home. But getting pre-approved for a mortgage can help you stand out from other hopeful buyers.

As an article from Wall Street Journal (WSJ) says:

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Pre-approval shows the seller you’re a serious buyer that’s already undergone a credit and financial check, making it more likely that the sale will move forward without unexpected delays or financial issues.

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. The more prepared you are, the better chance you have of getting the home you want. Connect with a trusted lender so you have the tools you need to purchase a home in today’s market.

written by KCM 9.26.2023

Your Home Equity Can Offset Affordability Challenges

Are you thinking about selling your house?

If so, today’s mortgage rates may be making you wonder if that’s the right decision. Some homeowners are reluctant to sell and take on a higher mortgage rate on their next home. If you’re worried about this too, know that even though rates are high right now, so is home equity. Here’s what you need to know.

Bankrate explains exactly what equity is and how it grows:

“Home equity is the portion of your home that you’ve paid off and own outright. It’s the difference between what the home is worth and how much is still owed on your mortgage. As your home’s value increases over the long term and you pay down the principal on the mortgage, your equity stake grows.”

In other words, equity is how much your home is worth now, minus what you still owe on your home loan.

How Much Equity Do Homeowners Have Now?

Recently, your equity has been growing faster than you might think. To help contextualize just how much the average homeowner has, CoreLogic says:

“. . . the average U.S. homeowner now has about $290,000 in equity.”

That’s because, over the past few years, home prices went up significantly – and those rising prices helped your equity to accumulate faster than usual. While the market has started to normalize, there are still more peo ple wanting to buy homes than there are homes available for sale. This high demand is causing home prices to go up again.

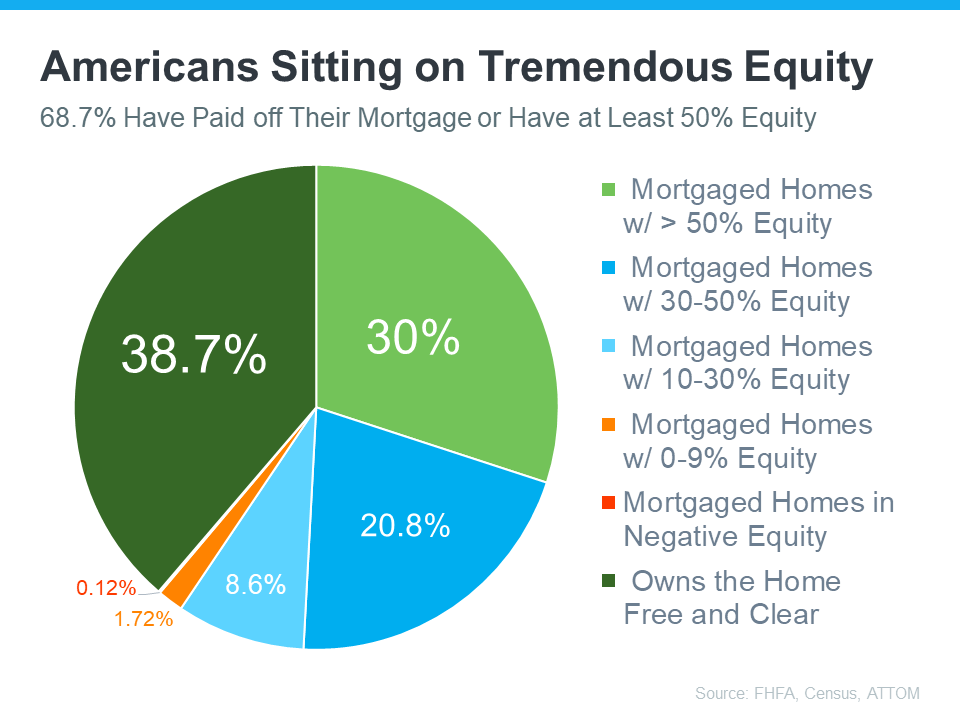

According to the Federal Housing Finance Agency (FHFA), the Census, and ATTOM, a property data provider, nearly two-thirds (68.7%) of homeowners have either fully paid off their mortgages or have at least 50% equity (see chart below):

That means nearly 70% of homeowners have a tremendous amount of equity right now.

How Equity Helps with Your Affordability Concerns

With today’s affordability challenges, your equity can make a big difference when you decide to move. After you sell your house, you can use the equity you’ve built up in your home to help you buy your next one. Here’s how:

- Be an all-cash buyer: If you’ve been living in your current home for a long time, you might have enough equity to buy a new house without having to take out a loan. If that’s the case, you won’t need to borrow any money or worry about mortgage rates. The National Association of Realtors (NAR) states:

“These all-cash home buyers are happily avoiding the higher mortgage interest rates . . .”

- Make a larger down payment: Your equity could be used toward your next down payment. It might even be enough to let you put a larger amount down, so you won’t have to borrow as much money so today’s rates become less of a sticking point. Experian explains:

“Increasing your down payment lowers your principal loan amount and, consequently, your loan-to-value ratio, which could lead to a lower interest rate offer from your lender.”

Bottom Line

If you’re thinking about moving, the equity you’ve built up can make a big difference, especially today. To find out how much equity you’ve got in your current house and how you can use it for your next home, let’s connect.

written by KCM September 2023

Three Things Buyers Can Do in Today’s Housing Market

It’s clear the 2022 housing market has been defined by rising mortgage rates. With rates on the rise, it’s also become more costly to purchase a home. According to the National Association of Realtors (NAR):

“Compared to one year ago, the monthly mortgage payment rose to $1,944 from $1,265, an increase of 53.7%.”

If you’re thinking of buying a home or have been trying to recently, that’s a big increase in a monthly mortgage payment – and it may be causing you to press pause on your plans. This jump is making homes less affordable, especially compared to the last two years when mortgage rates were at historic lows.

The good news is you can navigate today’s housing market and this rising rate environment with a few simple tips. Here are three things you may want to consider helping make your homeownership goals a reality.

1. Expand Your Search Area and Criteria

If you’ve been looking for a home in the city center or a specific area that’s starting to feel out of your price range, you may want to try looking a little further out in a location that could be more affordable. Expanding your search location or re-prioritizing the items on your wish list can open up opportunities you haven’t considered, and that could help you afford more of what you need (and want) in a home. As CNET notes:

“Area growth is likely to keep pace with the market, which means that the outskirts of town might be hopping within five years. Consider stepping out of your ideal location by searching in the nearby cities. You may find better prices and more square footage.”

2. Explore Alternative Financing Options

Working with a trusted lender to learn about the different loan types and options is essential too. According to Nerd Wallet:

“A variety of mortgages are available with varying down payment and eligibility requirements.”

Experts know how to point you in the right direction when it comes to exploring ways to find the best home loan for your situation. With rising mortgage rates making it more costly to finance a home today, there may be an ideal option out there your loan officer can introduce you to. This could make a home purchase more affordable and within your financial reach over the life of your loan.

3. Look for Grants, Gift Funds, and Down Payment Assistance

There are also many options available when it comes to securing the funding you need to purchase a home. One valuable resource to explore is downpaymentresource.com. Searching for specific down payment assistance options available in your local community could be a game changer when it comes to taking your first step toward homeownership. As NAR indicates:

“Many local governments and non-profit organizations offer down-payment assistance grants and loans, targeted to area borrowers and often with specific borrower requirements.”

Plus, there are programs and special benefits for individuals working in certain professions or with unique statuses, including teachers, doctors and nurses, and veterans.

Ultimately, that means there are many federal, state, and local programs available for you to explore. The best way to do that is to connect with a local real estate professional and your lender to learn more about what’s available in your area.

Bottom Line

If you’ve been searching for a home and have found yourself stepping out of the process because you’re worried about rising costs, let’s connect. Having a team of local advisors on your side may be just what you need to guide your search in a new and more affordable direction.